To LBP or not to LBP?

A comprehensive overview and analysis of the LBP landscape on FjordFoundry.

Lack of early investment opportunities for retail investors has been a persistent issue, while private capital has thrived on abundance. Attempts have been made to democratize the access to these early-stage ventures, but to what avail?

Introduction

Possessing adequate resources plays a pivotal role in a project’s debut plan. Means of securing funding and subsequently introducing a token to the open market are many and varied, each with their unique advantages and drawbacks. Venture backing is frequently sought after but remains inaccessible for most. Alternatively, launchpads or other crowdsourcing platforms are used to tap into external capital. FjordFoundry has been a popular choice among builders for quite some time, attributed to its reputation and robust platform. Through liquidity bootstrapping pools (LBPs), many protocols have entered the market with a solid cash injection to boot.

The high level objective of this post is to conduct an objective overview of vetted token offerings facilitated on FjordFoundry V2 and their price actions after initial sales have concluded.

All Eyez on LBPs

Prior to analyzing any tokens spawned from the protocol, a handful of important details need to be taken into account in order to be aware of unique dynamics associated with Fjord.

Specialist Endorsement

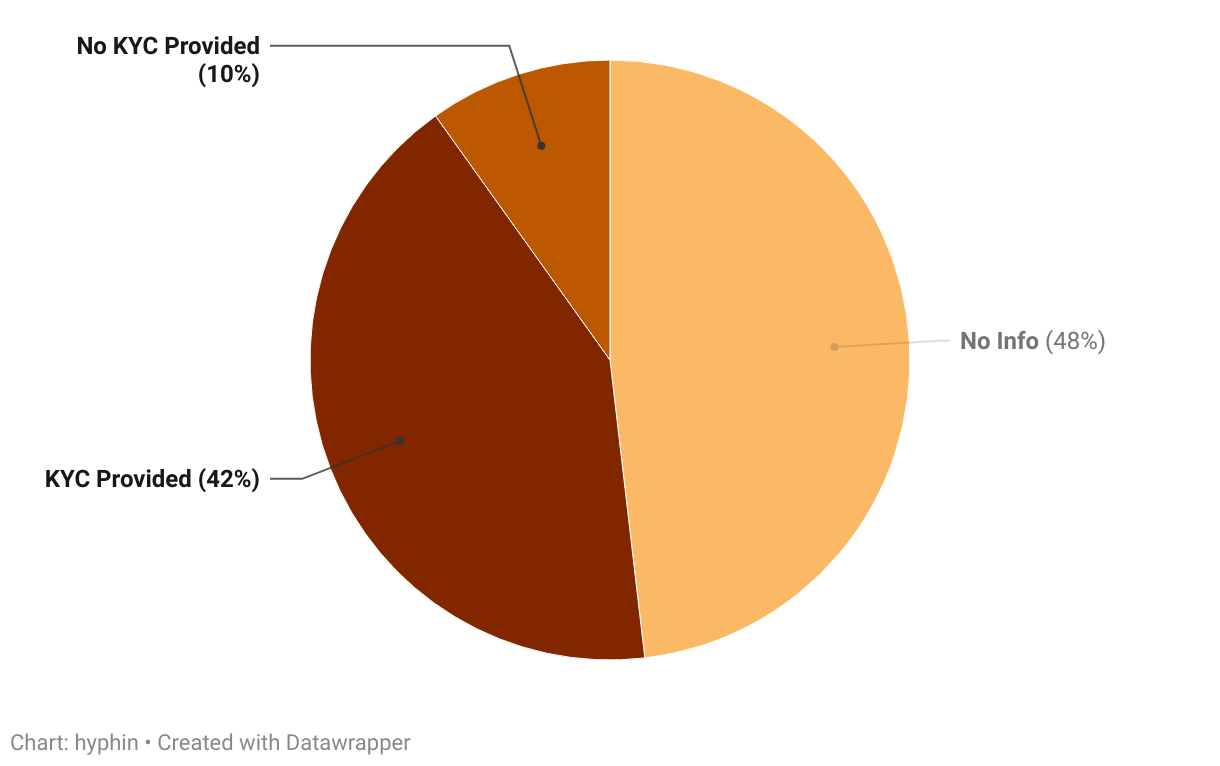

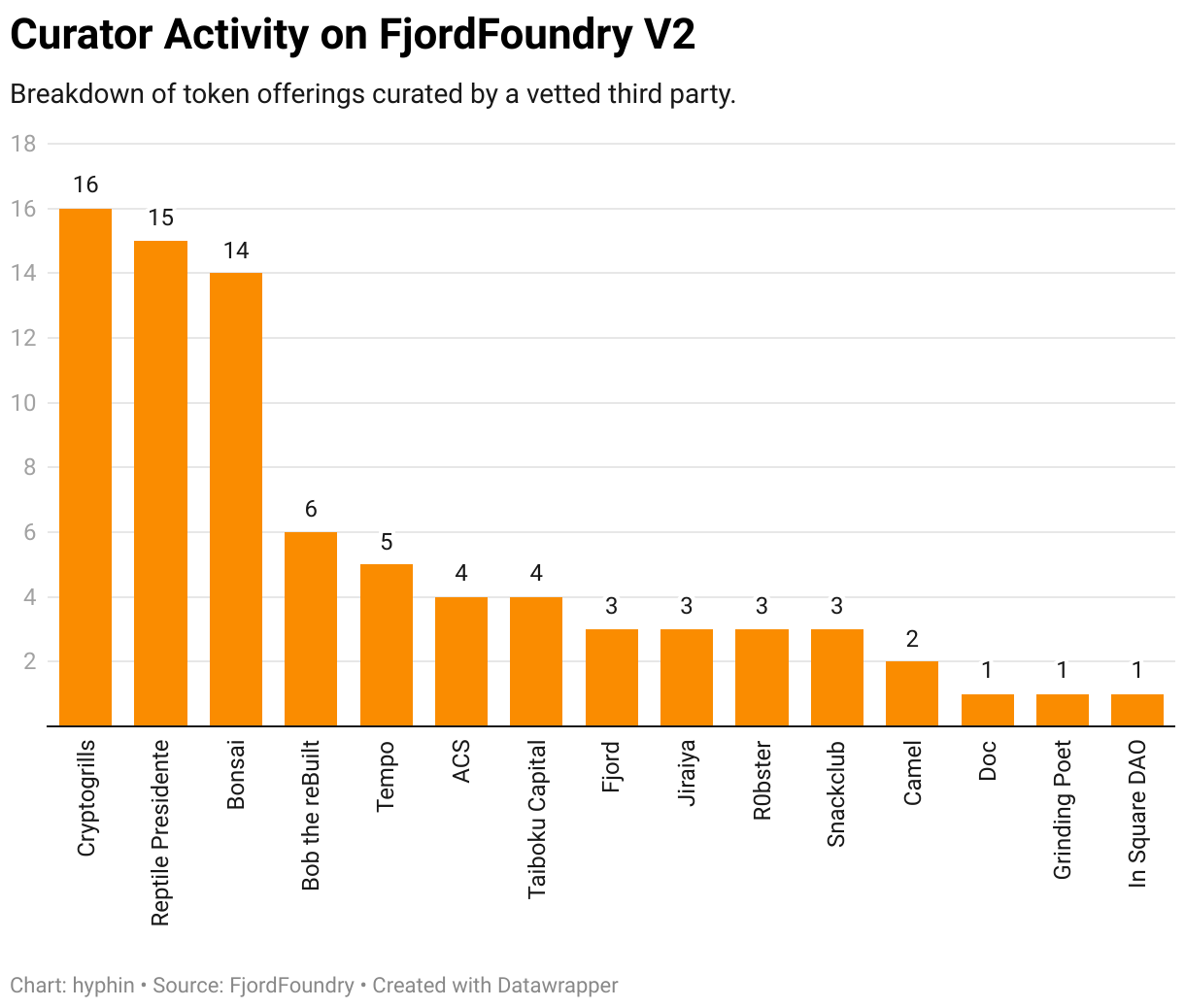

In a bid to invoke trust and enhance visibility on a permissionless platform, Fjord has hand-picked a group of knowledgeable individuals specializing in a variety niches to curate token sales.

4 out of every 5 projects on FjordFoundry V2 are curated.

Aside from representation, curators also might offer marketing or advisory services if necessary. Applicants looking to get their project curated, can expect to provide personal identification or any other relevant information required by the endorser for the sake of transparency and hold relevant parties accountable in the case of malicious behavior.

Due to changes in the user interface over time, some past sales don’t display any public information pertaining to KYC statuses as they weren’t logged at that time. Although in recent offerings, a large majority of the projects have a doxxed team.

Activity for curators varies, with some taking on more sales than others.

These vetted third parties are compensated with project tokens, sourced from swap fees generated during sales. Meaning that they’re directly incentivized to garner a lot of interest and ensure a well-attended launch.

Hastiness is Futile

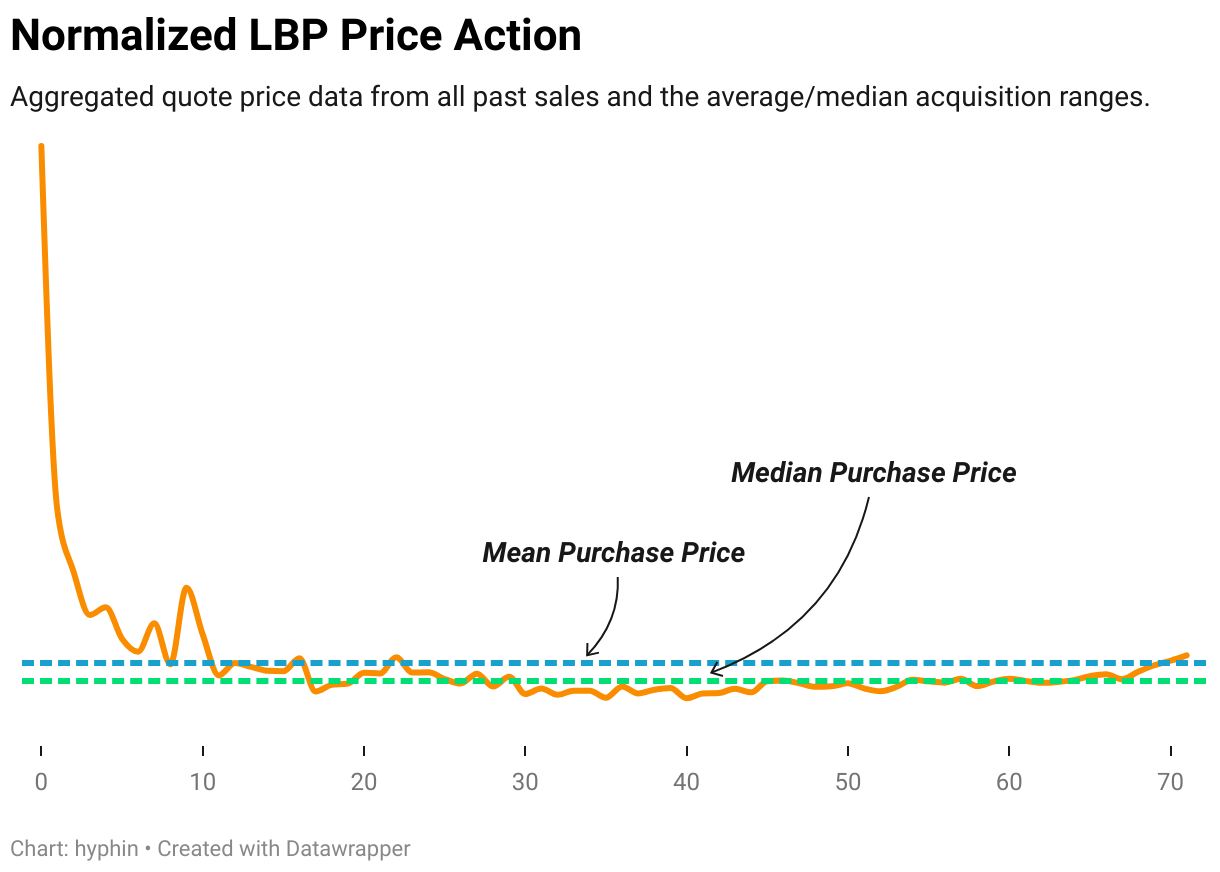

Contrary to fair launches and initial exchange offerings, being early does not pay off in the realm of LBPs. To promote equitable token distribution, a high-to-low pricing strategy with dynamic token weight shifting is employed to prevent price manipulation and other undesired behavior from bad actors.

By aggregating data from all past token offerings, we can can portray an average scenario to visualize how asset pricing tends to unfold and what the most common acquisition cost ranges are.

In most instances, prices remain relatively consistent after the 12 hour mark, only showing signs of stronger demand towards the tail end of the sale. Average and median cost bases highlighted on the chart indicate that most participants share similar entries, proving the concept this pricing model is trying to achieve.

Behind the Scenes

It’s important to be mindful of private rounds for marketers and strategic partners being held prior to a sale, with early contributors receiving tokens at a discount. Information regarding these sales are occasionally included in the Transparency section of the token page.

1 out every 4 curated projects has publicly displayed vesting details.

Data from sales with disclosed terms in addition to anecdotal evidence on Twitter and pitch decks floating around Telegram chats suggest the following being frequent occurrences:

Glossary:

TGE - Token Generation Event

Cliff - time period after which locked tokens will start to be distributed on a scheduleExample #1 ~ Aggressive

* Vested Tokens Released at TGE: 20%

* Cliff: 1 month

* Vesting Duration: 3-6 months

Example #2 ~ Conservative

* Vested Tokens Released at TGE: 0%

* Cliff: 3 months

* Vesting Duration: 4-12 months

Example #3 ~ Fjord Average

* Vested Tokens Released at TGE: 26.25%

* Cliff: N/A

* Vesting Duration: 8.53 months

Example #4 ~ Fjord Median

* Vested Tokens Released at TGE: 15%

* Cliff: N/A

* Vesting Duration: 7.46 monthsPrivate Round Discounts to Historical Fully Diluted Values

* Average: 33.4%

* Median: 60.22%

(Disclosed terms on Fjord as used as reference)The value that these vested parties provide and the impact they could have on price action is hard to determine, though legitimate projects usually try to include individuals who are more aligned with the team’s long-term vision and don’t use their audience as exit liquidity.

The Aftermath

Turnouts for token offerings are heavily dependent on the narrative being sold and getting the word out on social media. Interest in upcoming tokens bootstrapping on Fjord is strong across the board, attracting a solid amount of unique participants.

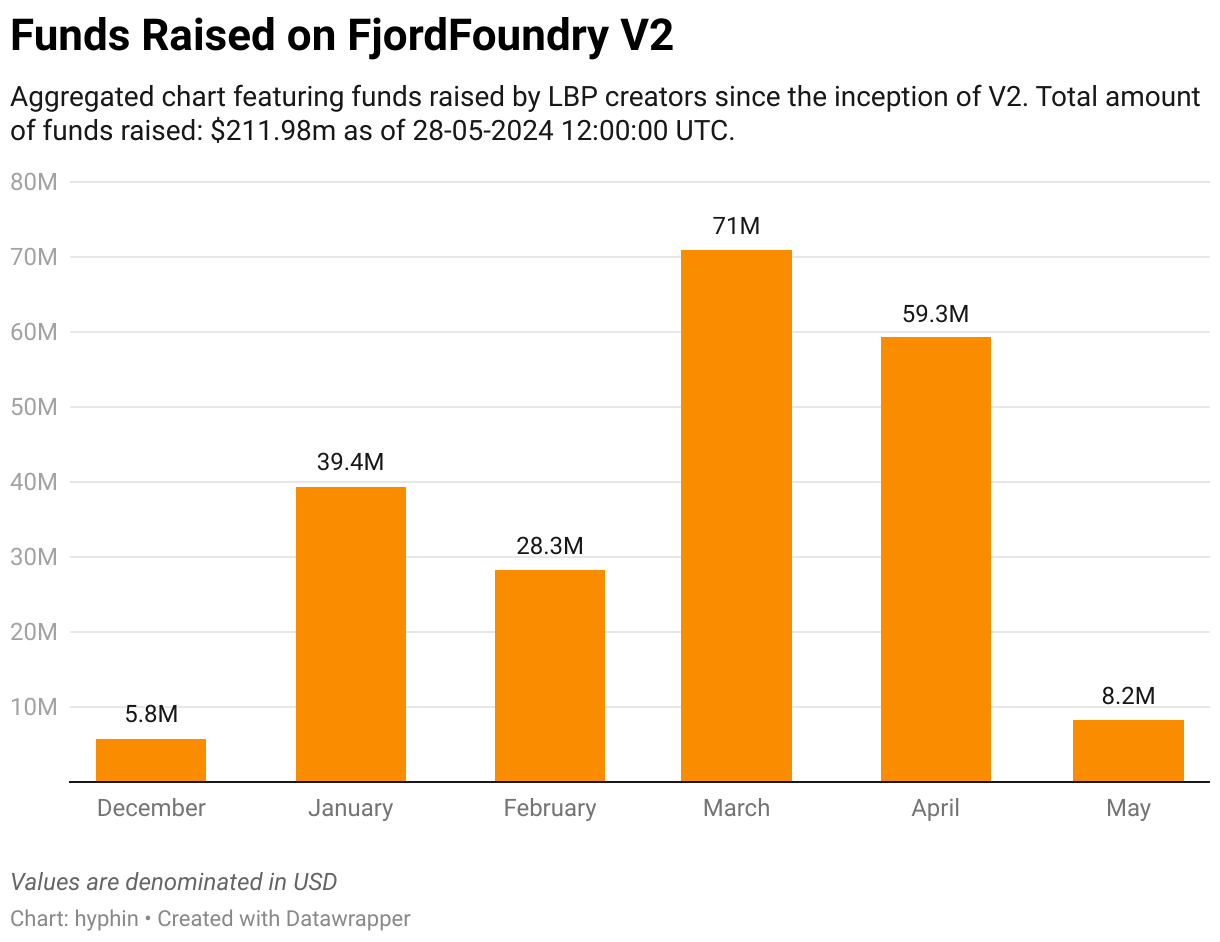

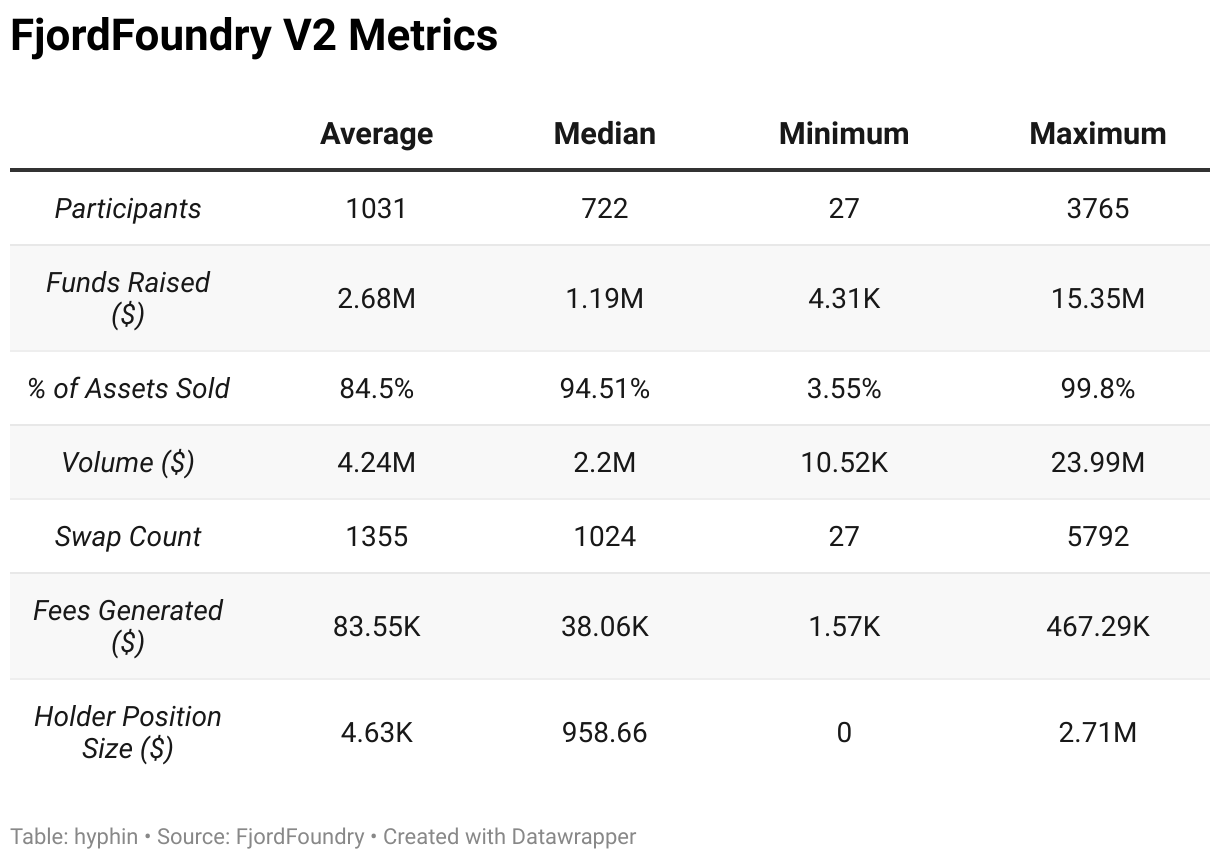

As of writing this article, 81 curated token sales have taken place over a six-month period. Data obtained from these events will serve as the basis for our analysis.

Usage metrics look very good as the sales tend to generate significant volume, protocol fees, and substantial capital for builders looking to get their projects off the ground.

This shows a lot of promise for teams seeking for funding, but how does this bode for the investors?

Price Performance

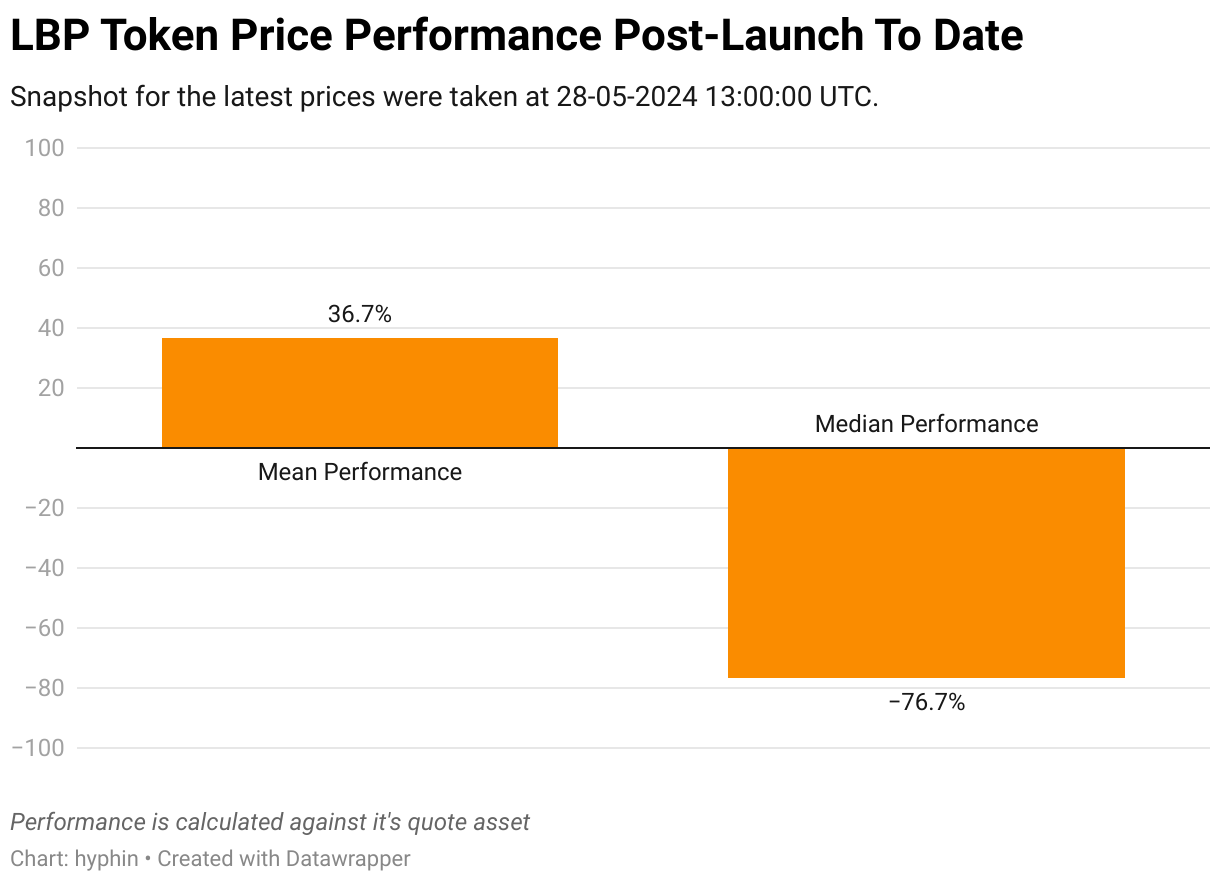

Token launches in general have proven to be a lucrative opportunity for speculators to turn a quick profit or secure long term positions at a favorable price. To determine whether this is the case for LBPs, final asset values on Fjord can be used as references against trading activity on decentralized exchanges to calculate average and median performances.

The massive disparity between the two metrics signifies that only a handful of tokens have yielded a positive return, with the rest incurring heavy losses.

~13.2% of tokens in the dataset are worth more now than they were before becoming available on decentralized exchanges.

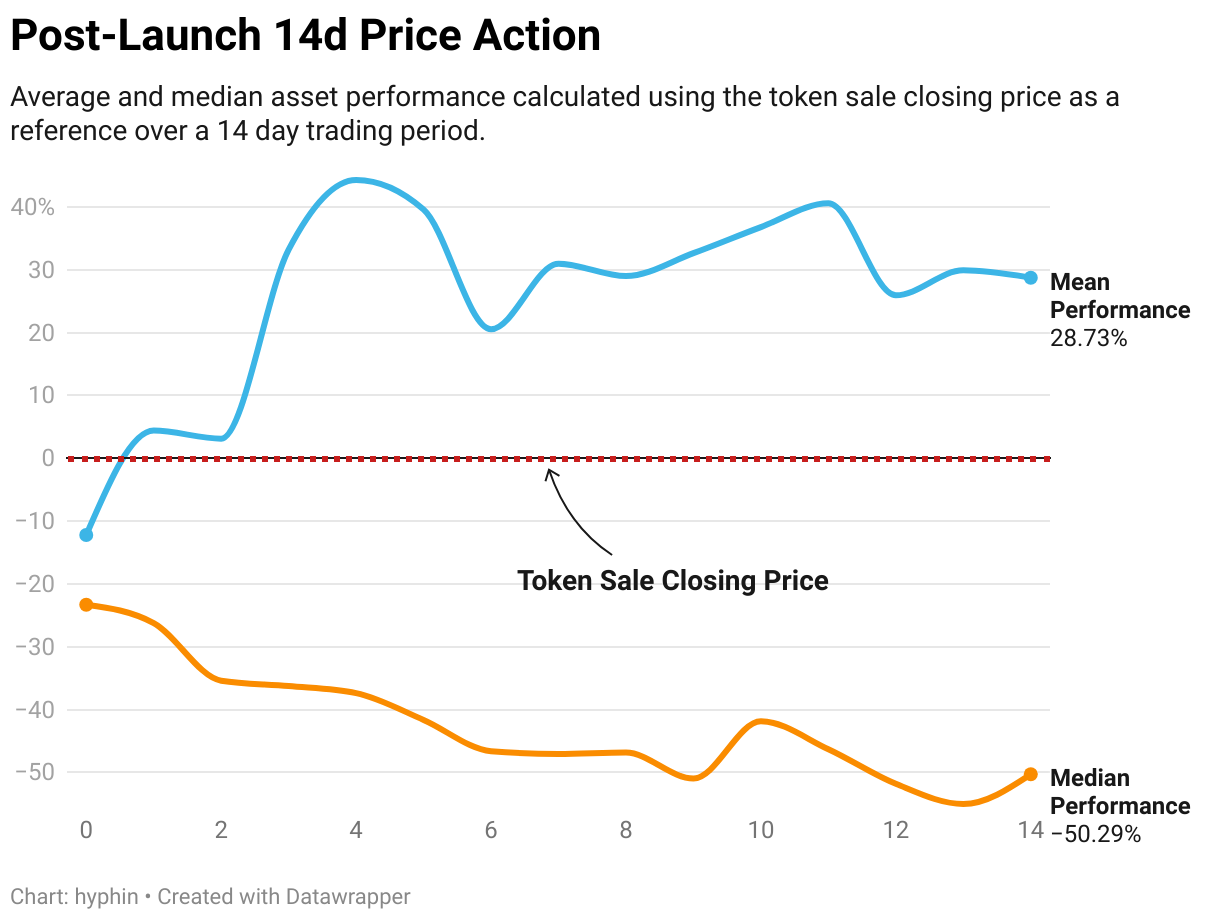

What constitutes this consistent negative performance? It’s hard to say for sure, but early-stage price action could hold some clues.

More often than not, the assets either launch at a discount or are immediately sold off, placing most early buyers deep in the red right off the bat. By observing what follows, it’s evident that sell pressure is rampant with buyers rarely stepping in to absorb it and tip the scales apart from a few cases where noticeable strength is present. Tracking wallet balances of those who participated in the token offering provides us insight into the forces shaping the charts.

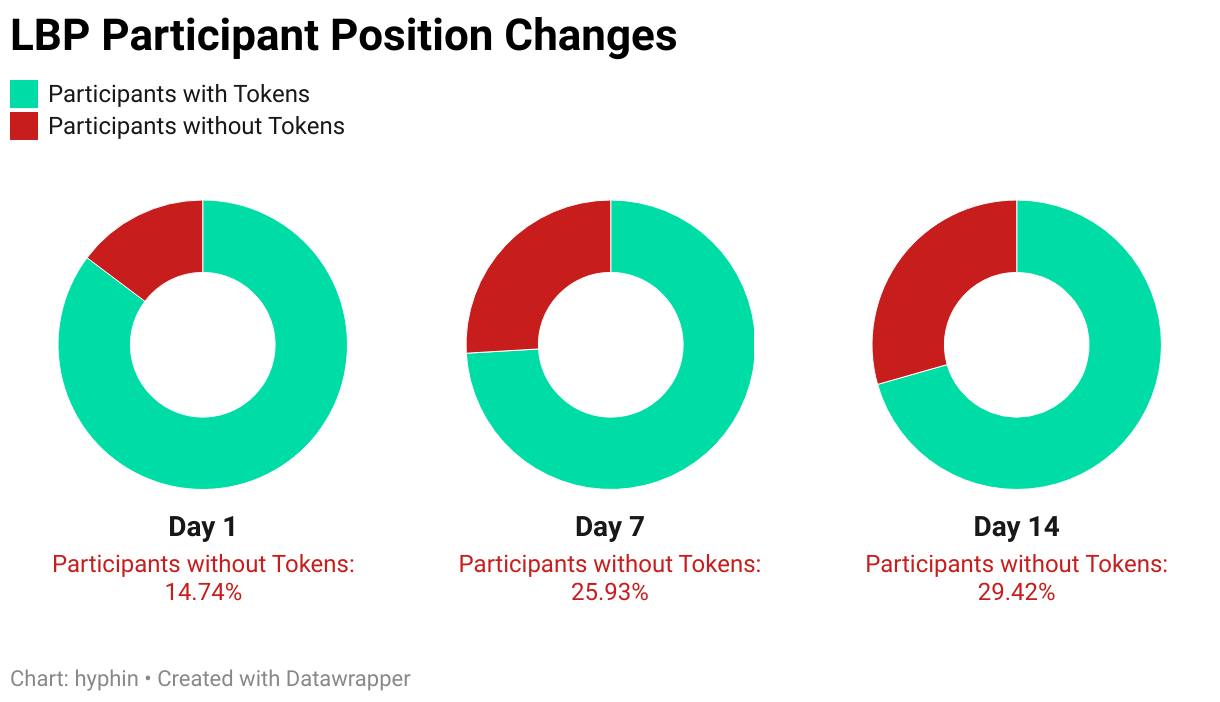

In the average scenario, nearly 15% of all LBP participants exited their entire position within the first day, with the percentage reaching 29.42% by the end of the observation period. This is inevitable and could be interpreted as the second distribution wave to onboard late entrants.

Inflated fully diluted valuations play a major role in these unfavorable situations playing out as the market just isn’t willing to catch falling knives made out of gold. Unless a fair value is found or enough interest from external parties is sparked, sellers will be in control until total exhaustion. Prolonged downwards price action could also be worsened by vested parties starting to cut their losses as the amount of unlocked tokens start to pile up over time.

A pitfall for many projects ends up being asymmetrical marketing efforts as a lot of emphasis is placed on the initial token offering on Fjord, but not on the aftermath. Ultimately leading to sky-high valuations that are difficult to sustain post-launch.

Takeaway

Visibility matters when it comes to token launches. Unattended venues are generally considered bad for optics, but don’t necessarily spell doom. While some assets might gather a crowd and initially be perceived as valuable, the fickle market has a tendency to dispute.

Disclaimer: The information provided is for general informational purposes only and does not constitute financial, investment, or legal advice. The content is based on sources believed to be reliable, but its accuracy, completeness, and timeliness cannot be guaranteed. Any reliance you place on the information in this document is at your own risk. On Chain Times may contain forward-looking statements that involve risks and uncertainties. Actual results may differ materially from those expressed or implied in such statements. The authors may or may not own positions in the assets or securities mentioned herein. They reserve the right to buy or sell any asset or security discussed at any time without notice. It is essential to consult with a qualified financial advisor or other professional to understand the risks and suitability of any investment decisions you may make. You are solely responsible for conducting your research and due diligence before making any investment choices. Past performance is not indicative of future results. The authors disclaim any liability for any direct, indirect, or consequential loss or damage arising from the use of this document or its content. By accessing On Chain Times, you agree to the terms of this disclaimer.