The CDP Narrative & the Evolution of Liquity Forks

An analysis of the CDP landscape, specifically Liquity and its ecosystem forks.

With the success and innovations brought forth by Liquity back in 2020, many developers have made use of it’s open source code base to make their own iterations of the original concept. In this article we will be discussing whether these derivatives had any significant impact on the market or not.

Introduction

Before we can talk about forks, we need to get familiar with some basic details about the underlying tech itself.

What is Liquity and how does it work?

Liquity is a decentralized borrowing protocol that allows users to borrow stablecoins issued by the platform in exchange for Ethereum.

What sets Liquity apart from other borrowing protocols?

Borrowers can take out zero-interest loans with a smaller collateral ratio compared to other platforms on the market.

How does Liquity generate revenue if the loans have no interest?

Liquity charges a small fee upon taking out a loan and when redeeming collateral from somebody else’s risky position with your stablecoins (not the same as paying back your loan).

Do they have a token?

Yes, Liquity has a token (LQTY). The tokens can be staked to receive fees generated by the platform.

What ensures the stability of this system?

The stability pool. It serves the purpose of absorbing and canceling debt from liquidated loans. Users are incentivized to deposit their stablecoins into this pool by offering liquidated collateral at a steep discount alongside native token emissions.

Bring out the forks!

Since Liquity only supports one collateral type and is designed to be relatively simplistic in order to minimize potential points of failure, builders saw an opportunity to expand on the idea by adding more collateral options and introducing novel mechanics.

Below is a flowchart that maps out all the prominent protocols stemming from Liquity’s original code.

All of these platforms sought out to bring something new to the table and on occasion served as a foundation for another product to be built on top of it.

The most popular and foreseeable design changes were the introduction of multiple collateral options and straying away from vanilla ETH. With the introduction of liquid staking tokens, it makes sense to provide users an option to borrow against a yield bearing asset in order to maximize capital efficiency.

Some unique attributes from platforms on this list that are worth mentioning.

Gravita

Their novel fee mechanic incentivizes short term borrowing by only charging a small borrowing fee when opening a position, which will be refunded if the debt is paid within six months (~182 days).

Prisma Finance

Prisma is offering depositors boosted yields on their positions by ve-locking their PRISMA tokens, similar to what can be seen on Pendle.

DeFi Franc

DCHF is the only protocol on this list, that has a non-USD stablecoin. In an industry where ~99% of the total stablecoin market cap is dollar dominated, they provided an alternative currency option to users.

Ethos Reserve

Most Liquity forks have a minimum debt requirement of $2000, but on Ethos Reserve users can easily borrow as little as $90 worth of ERN.

Lybra

In both iterations interest bearing stablecoins are issued with no minting fees and have an APY of ~8%.

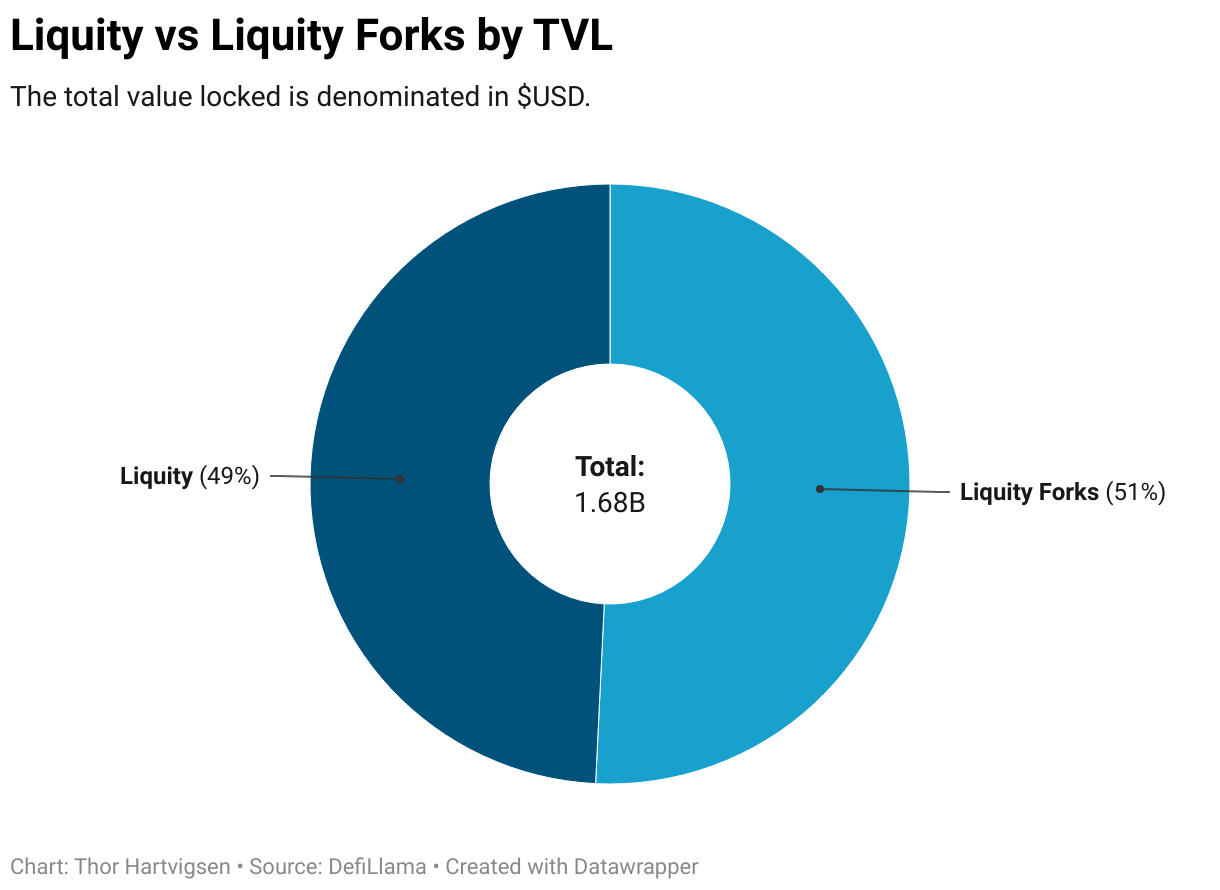

Does the market care?

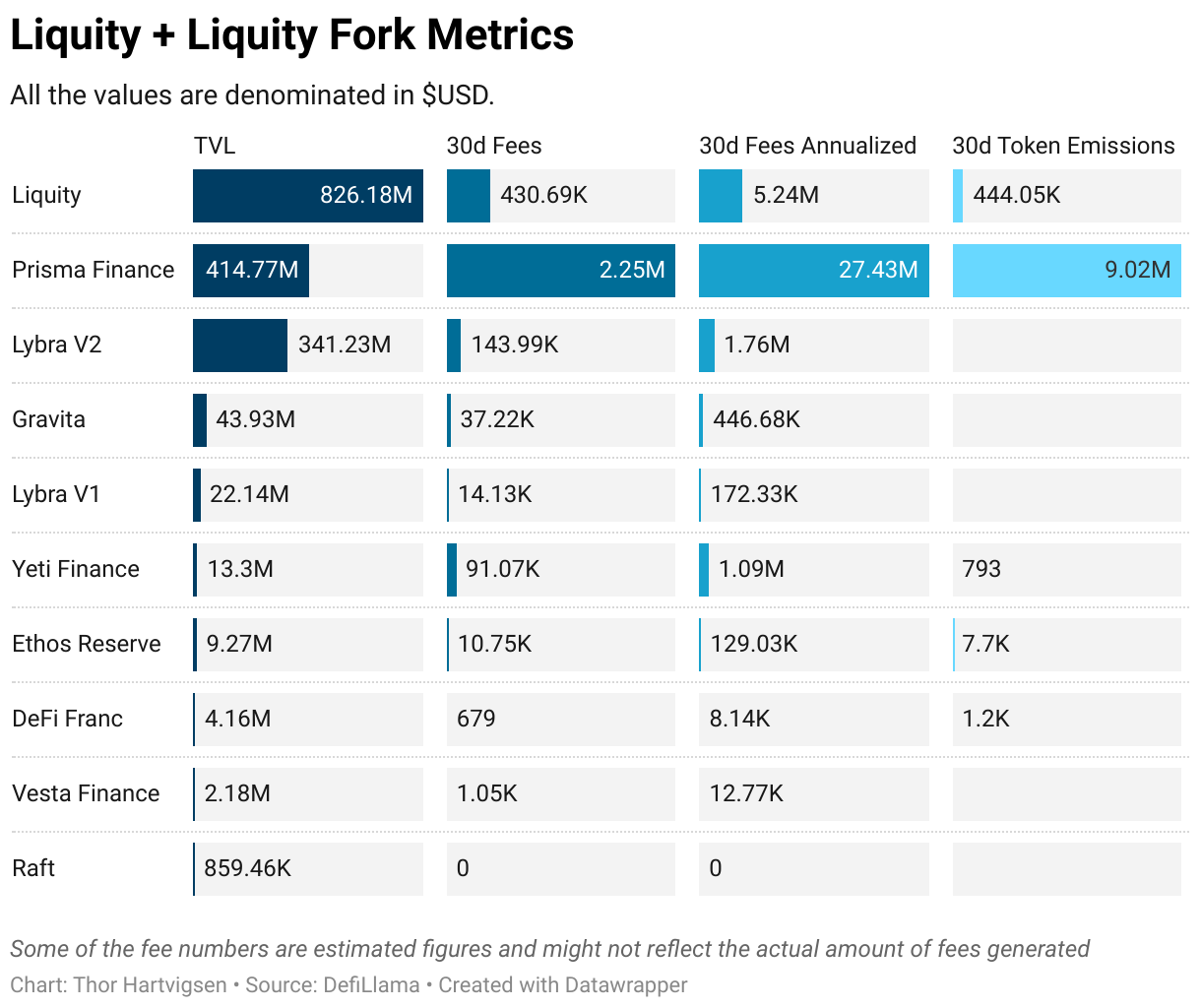

Liquity in theory should be the top choice for borrowers as its concept is solid and proven to be stable even in the worst market conditions. The most accurate way to confirm this is by looking at the allocation of capital in the space.

Surprisingly enough there is significant demand for the forks, with their cumulative TVL surpassing Liquity’s by a slight margin. The reason behind this flippening is due to newer platforms accepting LSD assets (e.g. stETH, rETH, cbETH) coupled with token incentive campaigns and additional functionality.

With this many options and a limited amount of liquidity, one would assume that only a handful capture majority of the market share.

That assumption is correct. It’s evident that most of the value locked is concentrated within the two most relevant protocols right now - Prisma and Lybra.

Based on the stats, Prisma is currently the premier of the forks. The sheer amount of fees it has generated in the last 30 days even shadows that of Liquity’s. With plans for revenue distribution, Prisma’s dominance will most likely keep increasing.

But why did some of the projects fail to garner significant value and remain competitive?

- saturation - due to a lot of these projects being similar in nature, users gravitate towards what is most popular or offers the most incentives;

- poor tokenomics - having inflationary ponzinomics invites mercenary capital that leaves as soon as rewards are tapered;

- bad marketing - effective marketing is a necessity when looking to attract new users or establish a presence in the space;

- no edge - not having a competitive edge in a saturated market guarantees minimal usage;

In Raft’s case, they were the victims of an exploit not too long ago. Fund recovery efforts are currently at play and the team is looking to make a comeback soon after revamping the back-end.

Conclusion

The market for these products remains fairly saturated when it comes to innovation, although there are a few solid projects that have risen to prominence and show great potential. Liquity still remains on the forefront for the time being, but will most likely be overtaken by another protocol in the near future as liquid staking tokens are being prefered more and more.