The Aladdin Ecosystem Overview 🧞♂️ - A hidden DeFi Gem?

Three protocols addressing three common wishes - good yields, product-market-fit and fair revenue distribution.

In the trenches of DeFi resides a community, shipping solid, clear-cut protocols focusing on providing value to depositors.

In this iteration of DeFi Frameworks, we will be covering products deployed by the Aladdin DAO and their current state in the market.

Introduction 💬

Since it’s inception in early-mid 2021, Aladdin DAO has a vision of creating high-performing financial products catered to yield farmers and users interested extracting the most out of their capital.

Through transparent and frequent communication with the community alongside incentives for contributors, Aladdin has built a loyal following.

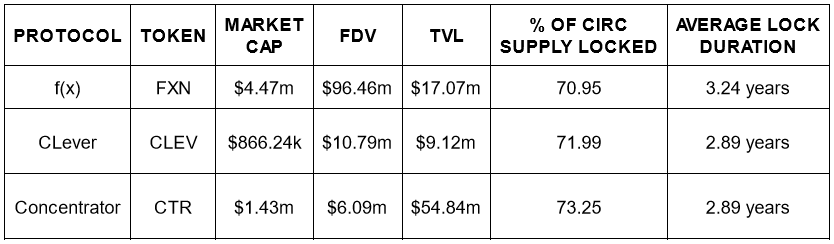

Their current line up consists of three protocols: Concentrator, CLever and f(x) Protocol.

Their initial two releases were aimed to find new approaches to yield farming optimization and automation within the Curve ecosystem. The latest deployment however, is branching out to explore scalable decentralized stablecoins.

Keep in mind that the Aladdin DAO owns 30% of the supply of each token and has permanently locked them, meaning that a portion of the revenue these protocol generate, flows back to their treasury.

At the moment, ALD stakers earn rebasing rewards with an APY of ~11%. Soon veALD will be deployed, which means that users ve-locking their token will start receiving a portion of the revenue earned by the DAO.

f(x) Protocol ❌

The suite’s shiny new gem, f(x) Protocol, allows users to convert their deposit into a synthetic low-volatility floating stablecoin or a high-volatility leveraged asset that has no funding fee or liquidations.

fToken

aka Fractional Token — decentralized low-volatility floating stablecoin that tracks 10% of the underlying asset’s price movements

xToken

aka Leveraged Token — decentralized long futures contract with varying leverage based on the ratio of xTokens present in the system (leverage lessens as the supply grows)

The platform at the moment only accepts ETH and stETH as collateral, but more assets will be qualified in the future.

Using Ethereum as an example, users can mint:

fETH (Fractional ETH);

fETH could be an alternative to holding stablecoins in a situation where USD devalues over time compared to ETH.In the last 90 days, fETH has delivered a better return than being flat and earning yield on USDC.

xETH (Leveraged ETH);

xETH could be useful for betting on the appreciation of Ethereum with a small amount of leverage, without incurring any funding fees or risks of liquidation in the case of a market-wide liquidation cascade.

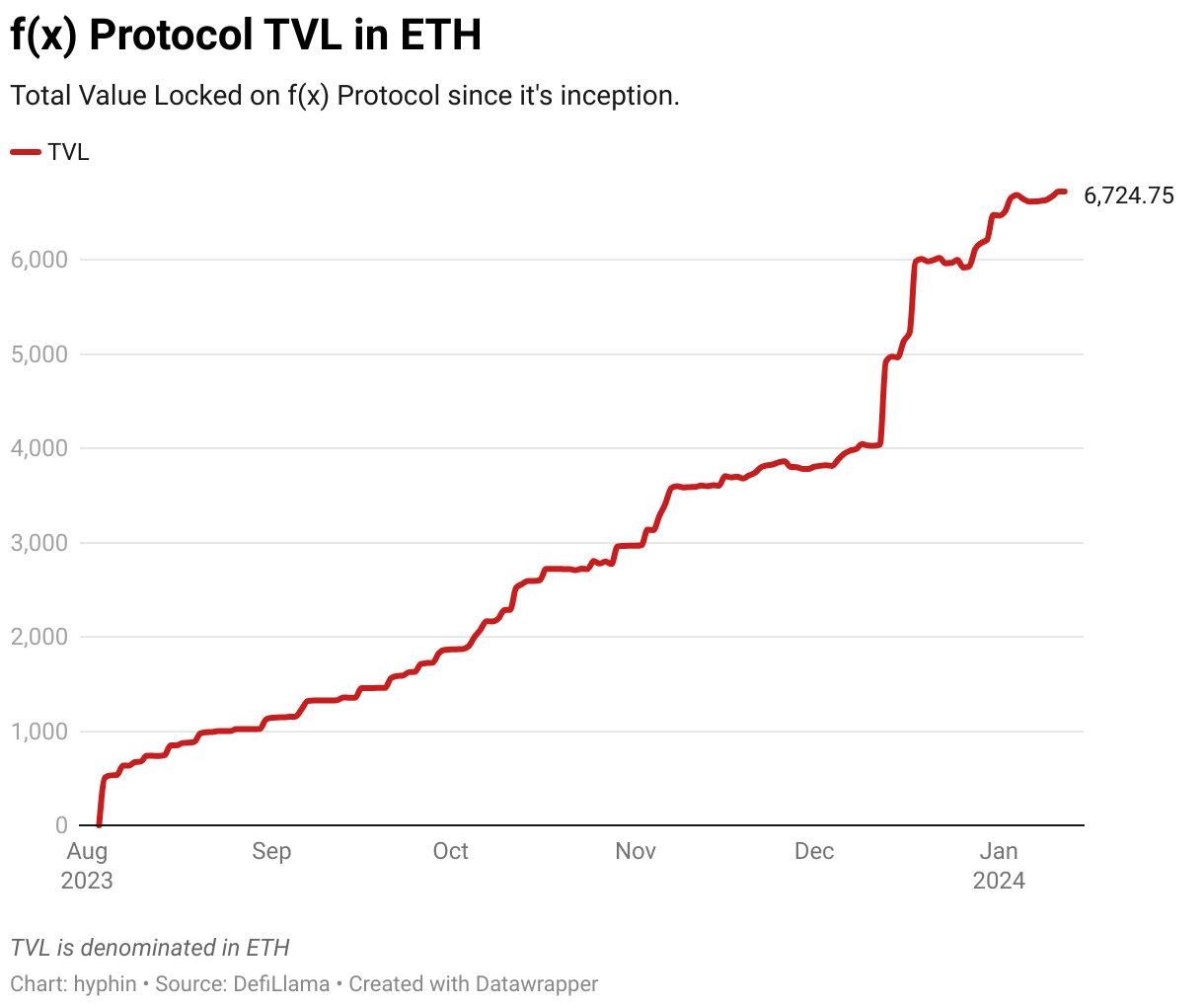

Interest in these tokens have been pretty obvious, considering the fact that the TVL has kept growing at a fast pace.

The TVL is expected to rise even more with no signs of stopping, as more upcoming developments are going to be implemented.

How is the system’s stability ensured?

If the TCR (Total Collateral Ratio) were to fall below 130%, the fTokens in the Rebalance Pool will be utilized for executing liquidation transactions. In the edge case of an insufficient amount of fTokens required to raise the TCR above 130%, temporary minting incentives will be put in to place. These incentives are funded by the treasury.

What is the value proposition of the platform’s token?

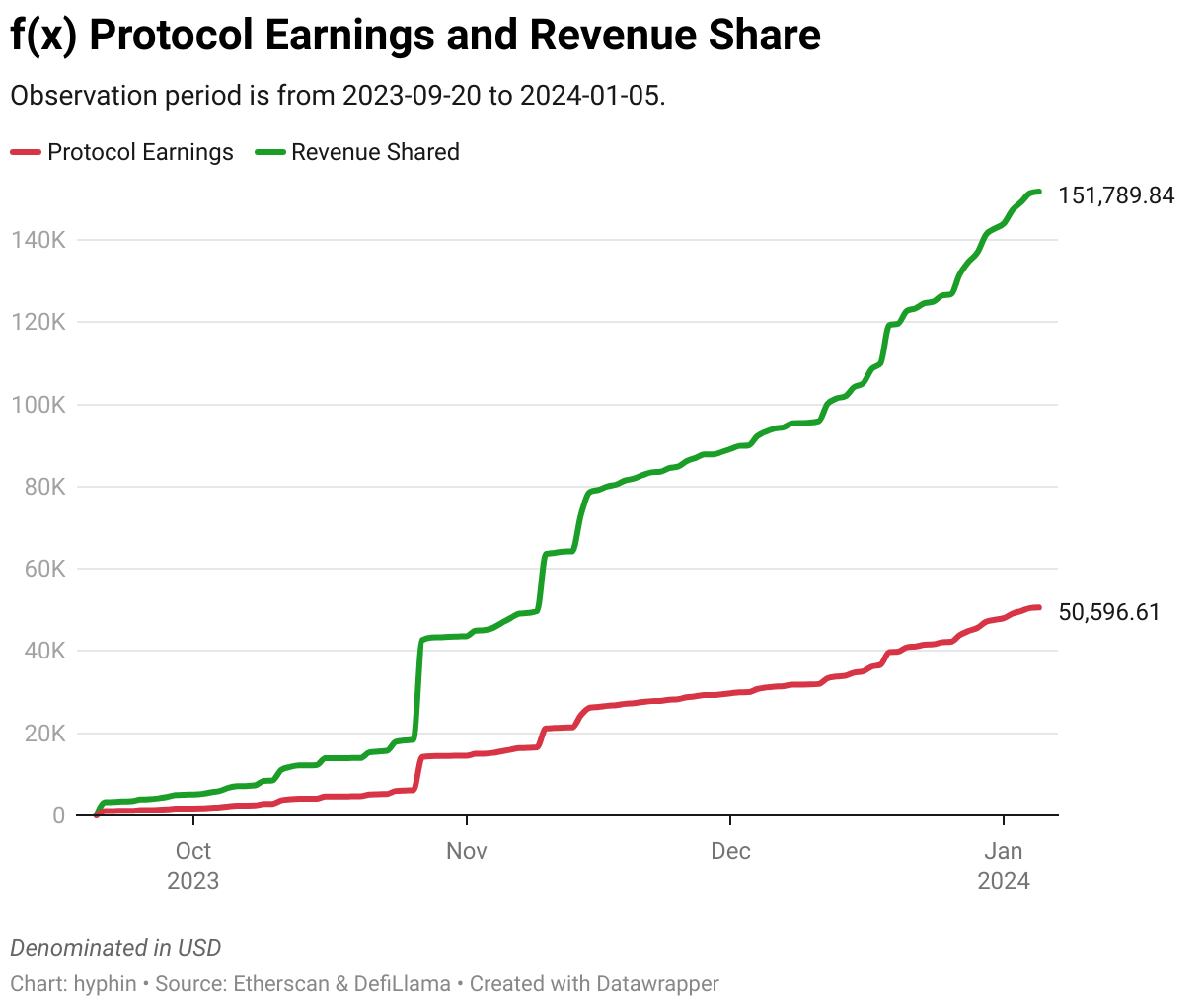

Adopting a ve-locking system similar to Curve, f(x) users have the opportunity to lock their FXN tokens to earn a 75% share of the total revenue generated by the protocol and also participate in governance proposals.

Are there any upcoming developments?

Aside from listing more f/x pairs, the team behind f(x) introduced the concept of fUSD, a hard pegged USD stablecoin in a governance proposal made not too long ago.

CLever 🔄

CLever is essentially a lending platform, that offers non-liquidating loans with the added benefit of being able to receive a portion of the future yield straight away.

clevTokens

Representing future yield in the form of a synthetic token, clevTokens can be claimed up to a specific percentage of the collateral value after making a deposit.

Yield Harvesting

Each collateral has it’s own yield harvesting mechanism. Harvested tokens are used to mint synthetic tokens against them and are distributed to depositors, granted they don’t have any debt, otherwise it’ll be used to pay back the loan.

The Furnace

A core system component, The Furnace is used to convert clevTokens back into real tokens.

Harvested tokens are placed into the furnace over a short vesting period (1-2 weeks), where they can be swapped for their synthetic token equivalent at a 1:1 ratio, after which they are burned.

However this conversion isn’t instantaneous, every clevToken has their own burn rate, which dictates how fast a synthetic asset is redeemed against a real one.

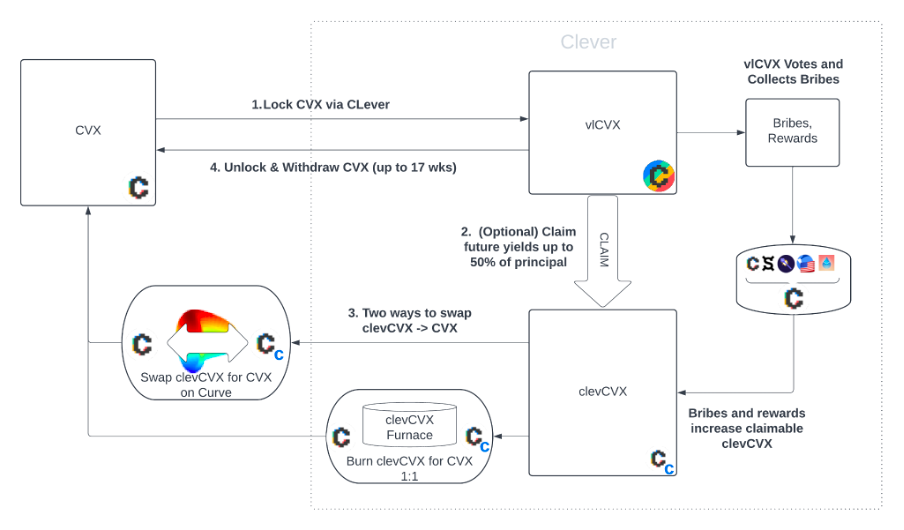

Now that we’ve covered all of the technical aspects, let’s take a look at how one would make use of this protocol. Below is an example of a yield strategy using CVX as collateral:

Using this strategy, CVX depositors can claim clevCVX and swap it for CVX on Curve to deposit back into CLever, creating a leverage loop. Since all of the deposited CVX tokens are automatically vote-locked, yield is generated from bribes and distributed back to the platform. Depositing clevCVX into The Furnace allows the user to convert it back to CVX over a period of time.

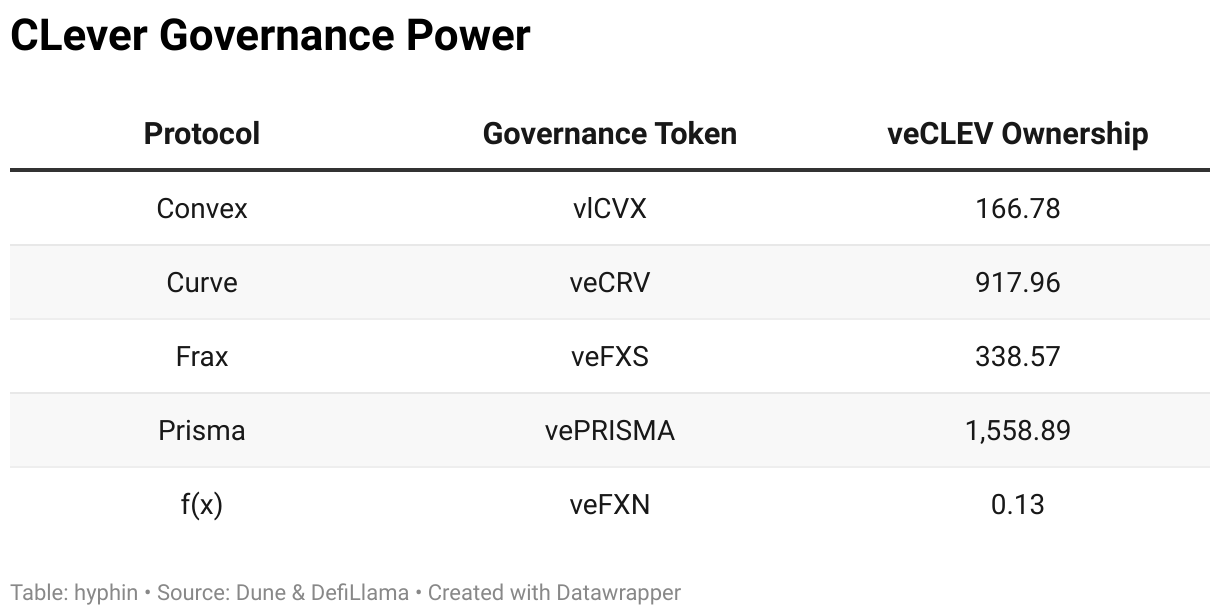

The Power of veCLEV

Due to it’s nature of being a CVX vacuum, veCLEV holders are entitled to a big say in governance proposals on various protocols.

Concentrator 🗜

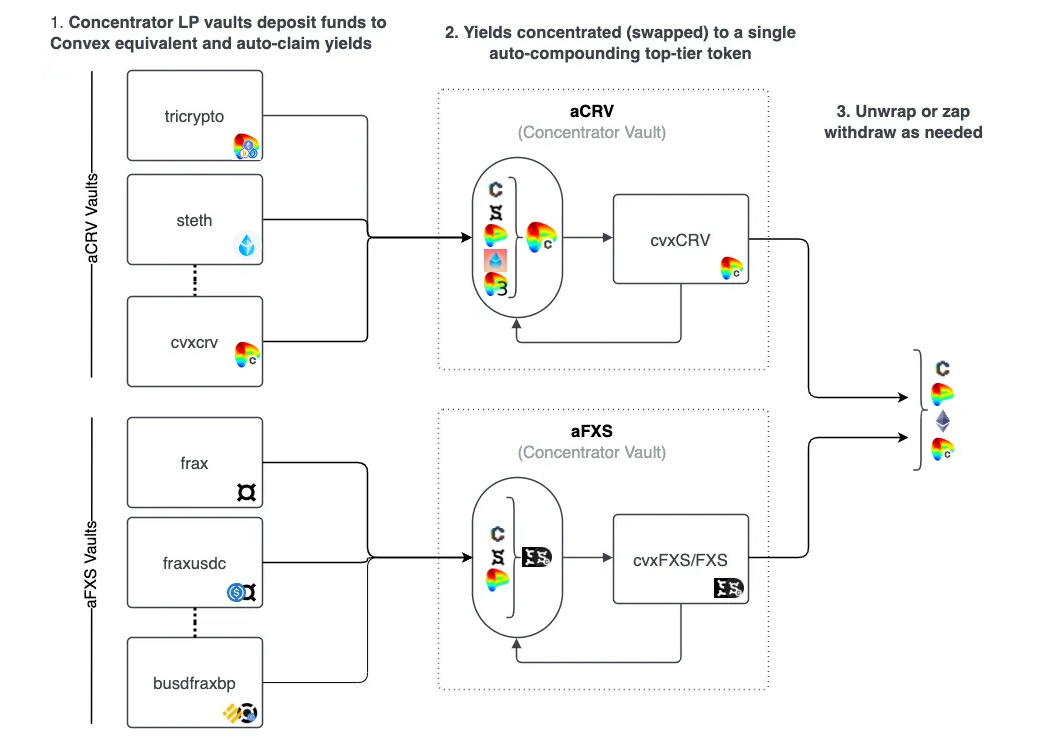

By leveraging the Convex and Curve ecosystems, in addition to efficient auto-compounding, Concentrator is able to offer enhanced yield to depositors all the while simplifying the process of yield farming.

As of now, there are 6 audited yield strategies available on the platform as vaults.

Vaults

These auto-compounding vaults work by placing the deposited assets into various Convex pool and then concentrating the rewards into the underlying token of the farming strategy.

aTokens

Wrappers representing a share of an auto-compounding Concentrator vault are called aTokens (e.g. aCRV or aFXS).

Below is an example, how the process looks like:

The deposited assets can be withdrawn at any time by either unwrapping the aToken or zapping out to other assets.

Concentrator is beneficial for yield farmers since it allows them to keep holding their desired LPs while earning rewards in another token. Not needing to spend additional gas fees to manually harvest rewards and then compound them improves capital efficiency.

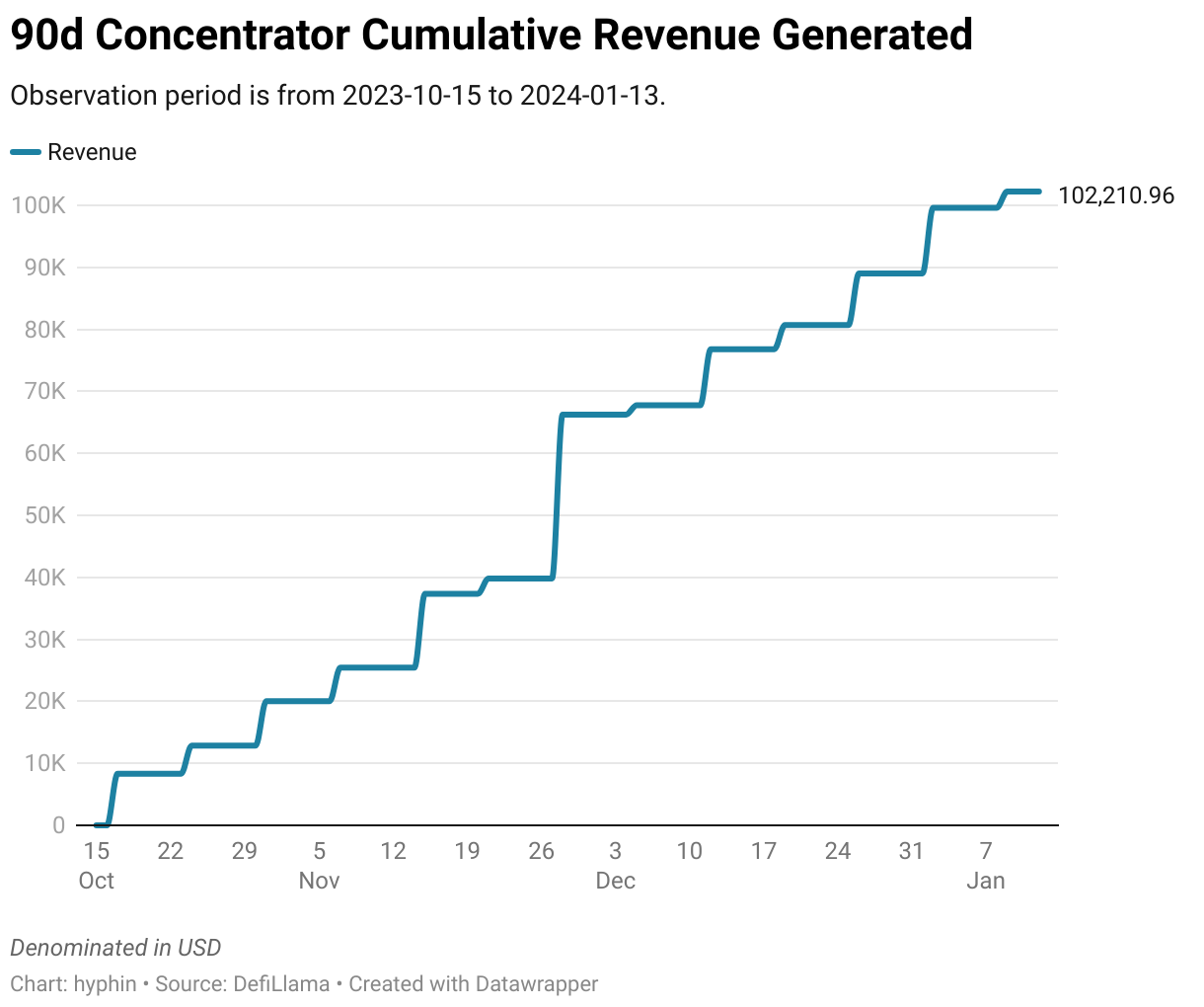

Despite it’s low market cap, Concentrator generates a considerable amount of revenue, half of which is distributed to veCTR holders in the form of aCRV.

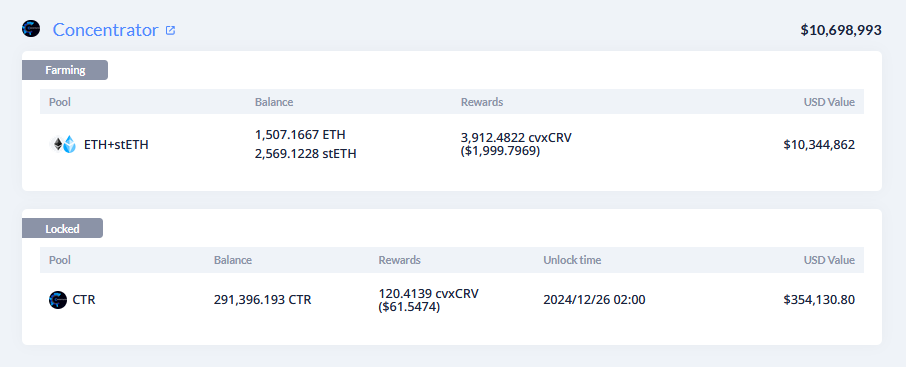

An individual with a wallet value of almost $35m and significant amounts of capital deployed to other Aladdin ecosystem projects, is leveraging Concentrator with size to earn of yield on their LP deposit without losing direct exposure.

Even locking up all of their tokens, this user is earning additional aCRV that is constantly compounding. For a full overview of the strategies performed by this wallet, see the tweet here.

Conclusion 🤔

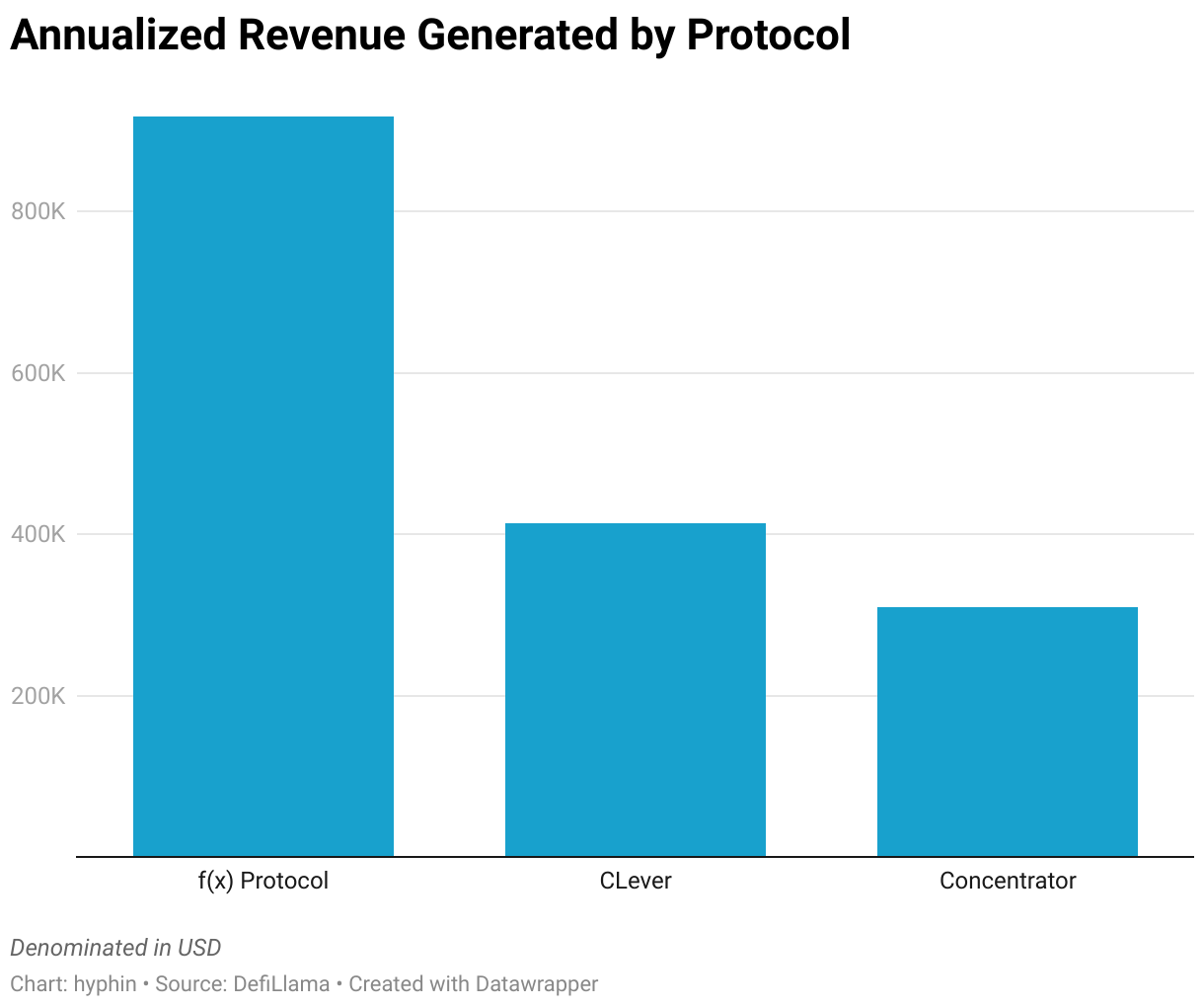

Other than offering useful services, the Aladdin ecosystem protocols post strong revenue numbers across the board and share at least half of it with ve-lockers.

As mentioned in the introduction, after the release of revenue sharing for ALD, people interested in the ecosystem can get exposure to all three of these projects rather than investing in them individually.

Even if the tokens themselves don’t appreciate by a big margin, long term lockers earn a solid yield.

All in all there is room for expansion as the ecosystem seems to be overlooked as a whole, increased visibility could attract more capital to these platforms and in turn generating more revenue which most likely leads to asset appreciation.

DISCLAIMER: The information provided in this document is for general informational purposes only and does not constitute financial, investment, or legal advice. The content is based on sources believed to be reliable, but its accuracy, completeness, and timeliness cannot be guaranteed. Any reliance you place on the information in this document is at your own risk. The document may contain forward-looking statements that involve risks and uncertainties. Actual results may differ materially from those expressed or implied in such statements. The author(s) of this document may or may not own positions in the assets or securities mentioned herein. They reserve the right to buy or sell any asset or security discussed at any time without notice. It is essential to consult with a qualified financial advisor or other professional to understand the risks and suitability of any investment decisions you may make. You are solely responsible for conducting your research and due diligence before making any investment choices. Past performance is not indicative of future results. The author(s) disclaim any liability for any direct, indirect, or consequential loss or damage arising from the use of this document or its content. By accessing this document, you agree to the terms of this disclaimer.