Marching Towards the Berachain Mainnet

In case you are still wondering whether Berachain is real or not. The definitive answer will be made clear in the coming months.

What started off as an inside joke between friends, has slowly but surely evolved into a novel, possibly game changing addition to the space. Ambitions of deploying an alternative consensus mechanism will soon be turned into reality.

Introduction

It’s common knowledge that there are more blockchains than people using them. The same however can’t be said about the methodology used to achieve a common state between participants on their decentralized ledgers.

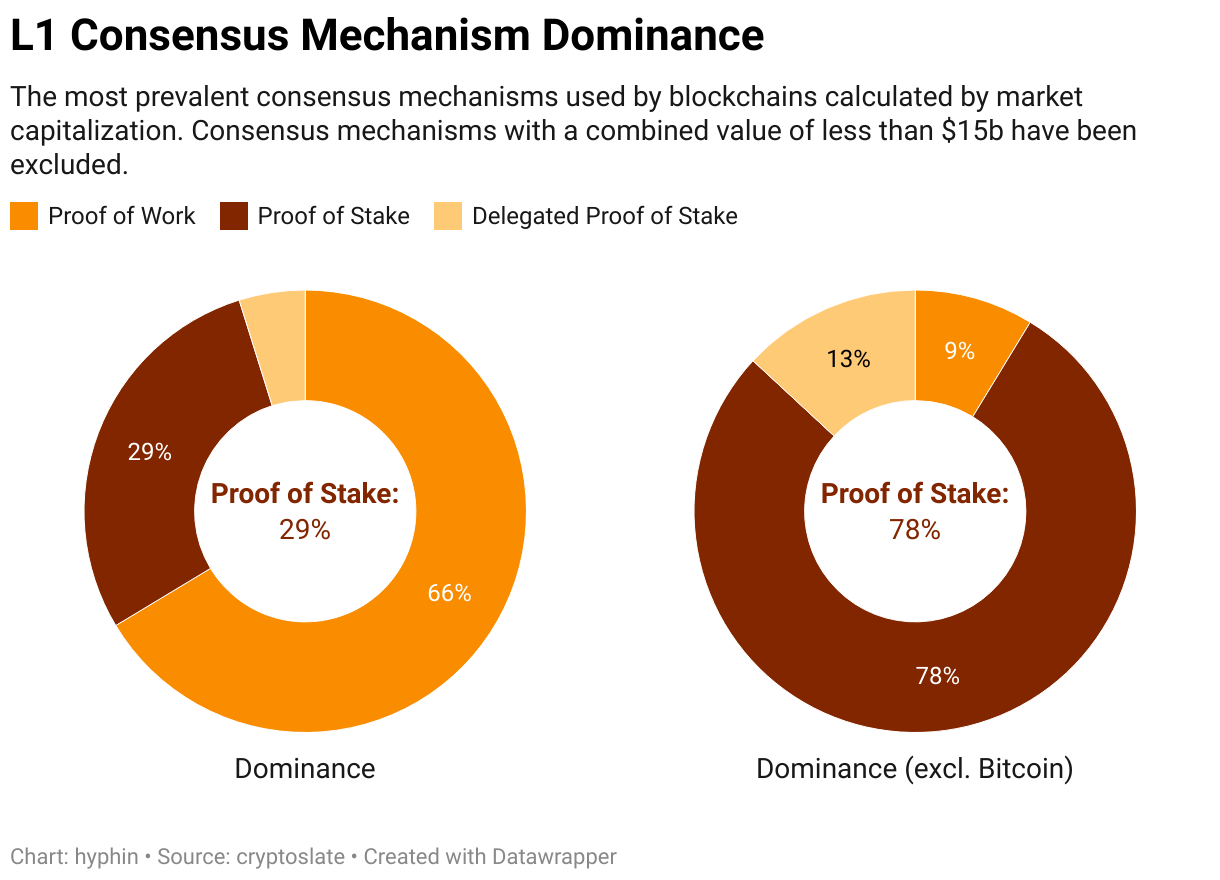

Most of the chains that we know and interact with on a frequent basis use either Proof of Work (e.g. Bitcoin), Proof of Stake (e.g. Ethereum) or Delegated Proof of Stake (e.g. Solana) as their consensus mechanism. Although not perfect, these systems have proven their reliability and security over time, hence the widespread usage amongst builders.

From time to time new designs do appear, but ultimately fail to capture a significant part of the market share and get snuffed out by their competitors. But there is a new kid on the block with their own take on blockchain governance up it’s sleeve, that has the potential to make a dent in the industry.

security = f(liquidity)

Despite the absence of an official marketing position, Berachain, an EVM compatible L1 built on the Cosmos SDK, has managed to generate a significant amount of buzz on Twitter. Memorable appearances at various events and on media platforms in addition to a community facing, builder friendly stance have proven the founding team to be extremely likable — a breath of fresh air from the usual corporate-esque, VC protocols we’ve seen many times in the past.

Differentiating themselves from competitors, Berachain has developed a new economic model, Proof of Liquidity, with the purpose of addressing concerns commonly associated with proof-of-stake networks:

- Governance Liquidity Vacuum;

Securing the network requires a large amount of liquidity that could otherwise be used in the ecosystem. Liquid staking derivatives do solve this issue to some extent, but introduce centralization risks in the process. - Misalignment between Protocols and Validators;

Protocols have little opportunity to improve the security of the chain they're building on, and validators receive minimal upside from the protocols that they run infrastructure for.

To make their vision a reality, a set of implementations have been put into place to achieve three major objectives.

A key component of their approach: securing the chain by maximizing on-chain liquidity, is made possible by modifying the tokenomics. Covering transaction fees and participating in governance, in most cases, is performed using the network’s native token. Berachain on the other hand separated the delegation token from the gas token, making each one serve its unique, individual purpose:

- BERA — native gas token;

- BGT — governance token;

Bera Governance Tokens can’t be transferred, bought nor sold. However, it is possible for them be burned in exchange for the gas token at a 1:1 ratio.

While seemingly unnecessary, this token design will make sense once we visualize the mechanism by mapping out the relevant processes and entities.

- Users providing liquidity to decentralized exchange pools are rewarded governance tokens.

- Governance tokens can be delegated to various validators present on the network.

- Validators produce blocks based on their proportional weight of governance tokens delegated to them.

- Validators direct future governance token emission across any number of liquidity pools through a configurer smart contract (BeraChef).

- Delegators can receive bribes from validators in case such an agreement exists.

Direct incentivization of providing liquidity through token emissions makes inflation distribution more equitable by rewarding individual market participants instead of a central authority. An abundance of liquidity and the option to direct future incentives through delegation introduces new dynamics to the on-chain ecosystem, encouraging validators and protocols to collaborate for mutual benefit.

This unfortunately only explains how governance tokens are emitted and distributed, but what about the gas token?

Upon initially launching the chain, addresses included in the genesis configuration file receive a predetermined BERA balance as soon as the first block is mined.

The starting block is mined by the coinbase address (more commonly referred to as the zero address or burn wallet), receiving the first block reward on the network.

After this has taken place, validators are incentivized to propose and validate new blocks by receiving block rewards and transaction fees in exchange for securing the network. So unless you’re lucky enough to be on the receiving end of an allocation or operating a validator node, the most probable means of obtaining tokens are either through applying for a builder grant, an airdrop, burning rewards received from providing liquidity, bribes or from an exchange after the mainnet becomes available.

Testnet Implementation

While the concept itself might show promise, what actually matters is the implementation. Does it attract users in a severely saturated market? Does it work as intended? Luckily for us the testnet has been live since early January, providing us some insights in regards to performance and usage. It’s worth mentioning that this is an experimental deployment with limited functionality and could be subject to change, so most observations should be taken with a grain of salt.

Activity

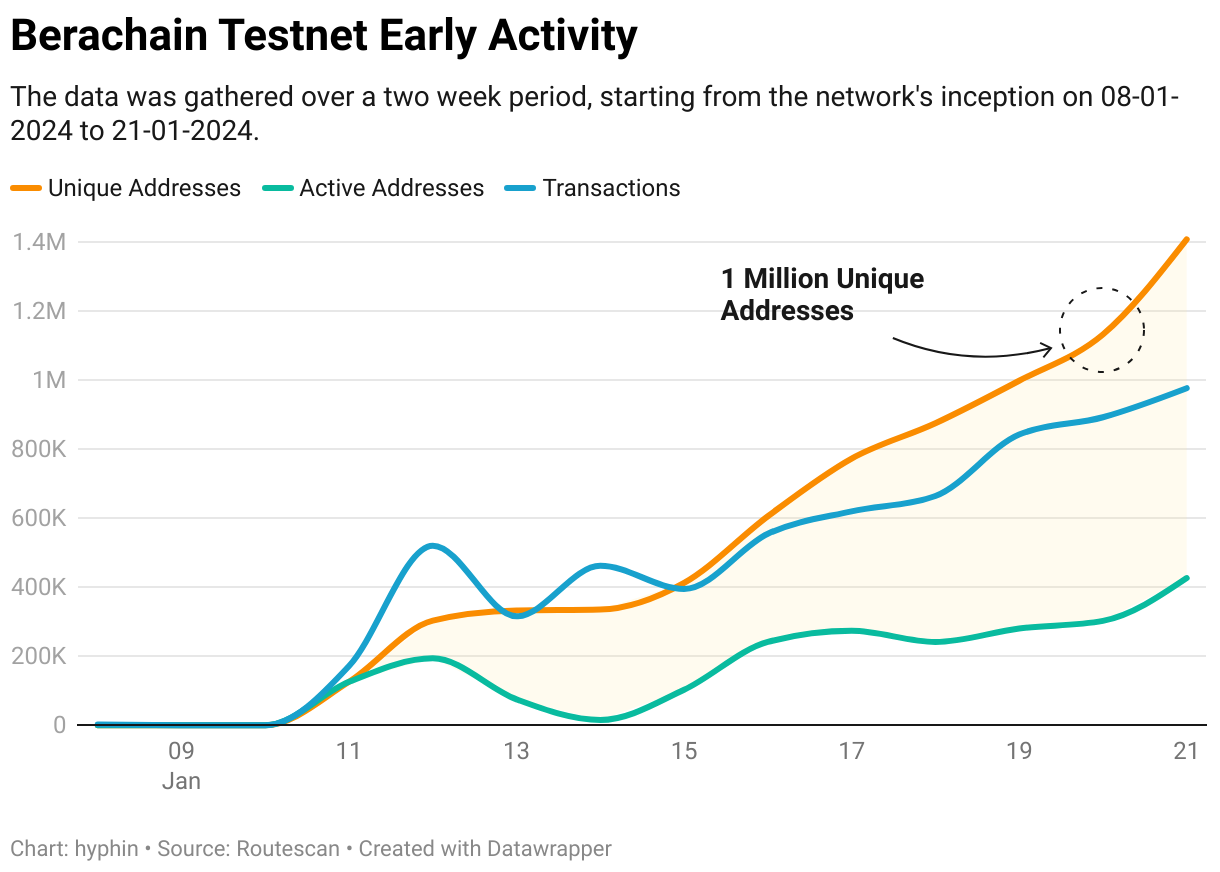

To get a glimpse of the initial interest in Berachain, inspecting post launch metrics should give us an idea how strong its pull was.

In just 12 days a cumulative amount of one million unique addresses were generated on the network, of which a fraction remained active. This phenomena is frequently seen when analyzing testnet usage metrics since the gas tokens are distributed through faucets that often times get abused by people automating the claiming process or doing it manually for multiple addresses. Initial congestion or RPC issues could have also played a role by barring users from interacting with the chain.

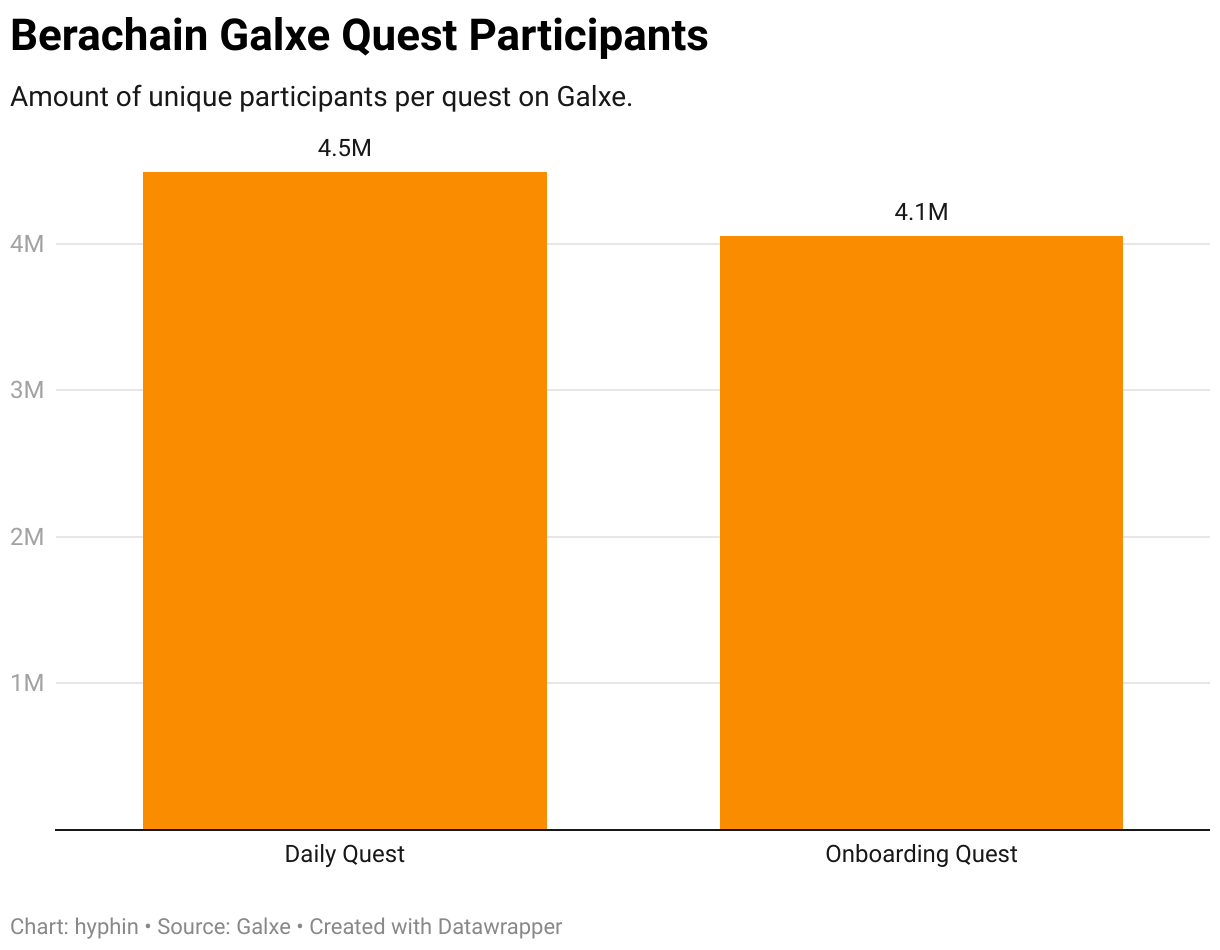

A strong force driving the impressive momentum was their 3 month long Galxe campaign that amassed more than 4 million unique participants per quest.

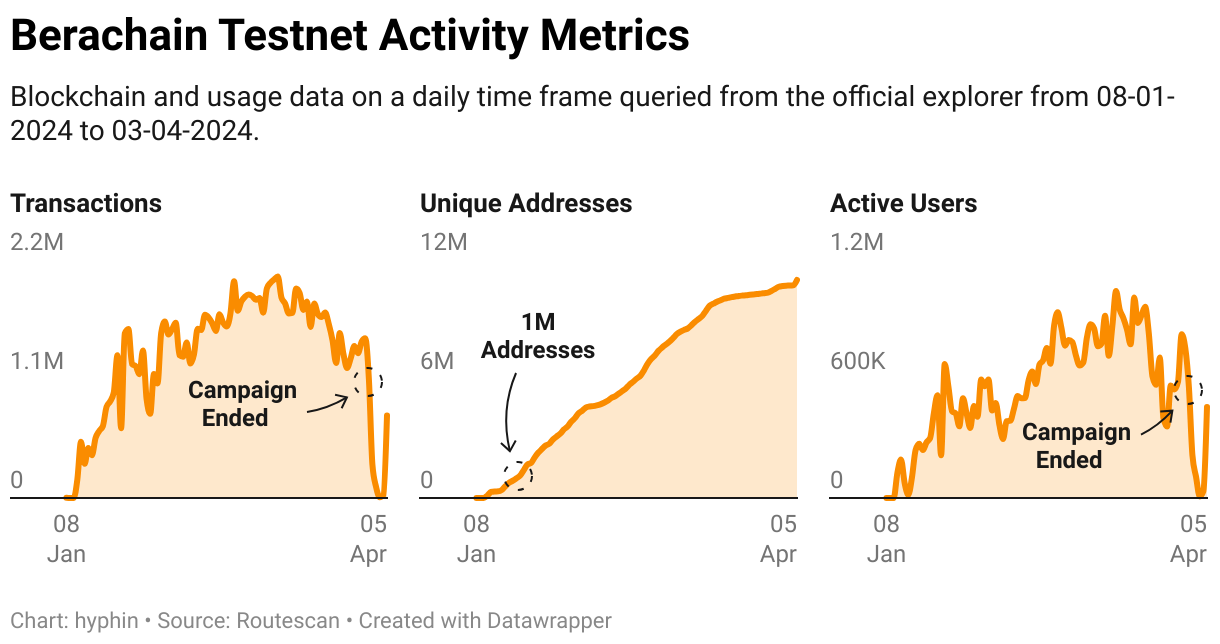

Zooming out and including recent metrics, it’s apparent that activity started to dwindle right around the time Galxe campaigns were concluded (31st of March). This behavior is expected since the testnet does not provide any actual value to users other than being rewarded for interactions.

EDIT (04-08-2024):

The abnormal reduction of activity could have been caused by indexing issues faced by the official Beratrail explorer. Metrics included in the chart above have started to change drastically after the post was published, with daily transactions being higher than they were on the 31st of March.

Ecosystem

As of now, there’s a myriad of protocols to explore on the testnet with new ones coming out on a daily basis, but we’ll be strictly be focusing on the Berachain native projects that are the sole emission receivers:

- BEX (Decentralized Exchange);

Unarguably the most important entity in the landscape. Deep liquidity is provided through a set of house pools that ensure efficient token swaps and serve as a foundation for future meta pools. These (meta) liquidity pools are comprised of at least one LP token, enabling greater capital efficiency by simultaneously providing liquidity in multiple pools. - Honey (Stablecoin);

Using USDC as collateral, users can mint (0.5% fixed fee) the chain’s native stablecoin HONEY with the optionality of later redeeming (0.5% fixed fee) the collateral. It is the most widely used stablecoin on Berachain and is integrated into most protocols. - BERPS (Perpetual Futures Exchange);

Forked from Gains Network, BERPS offers up to 100x leverage with a minimum notional position size of 10 HONEY across four different trading pairs: BTC-USDC, ETH-USDC, TIA-USDC and ATOM-USDC. Users can also stake HONEY to receive a portion of the trading fees generated by the protocol. - BEND (Borrowing/Lending Market);

WBTC and WETH can be used as collateral to borrow HONEY while receiving BGT emissions. HONEY can also be supplied to earn interest yield. The protocol is an AAVE fork.

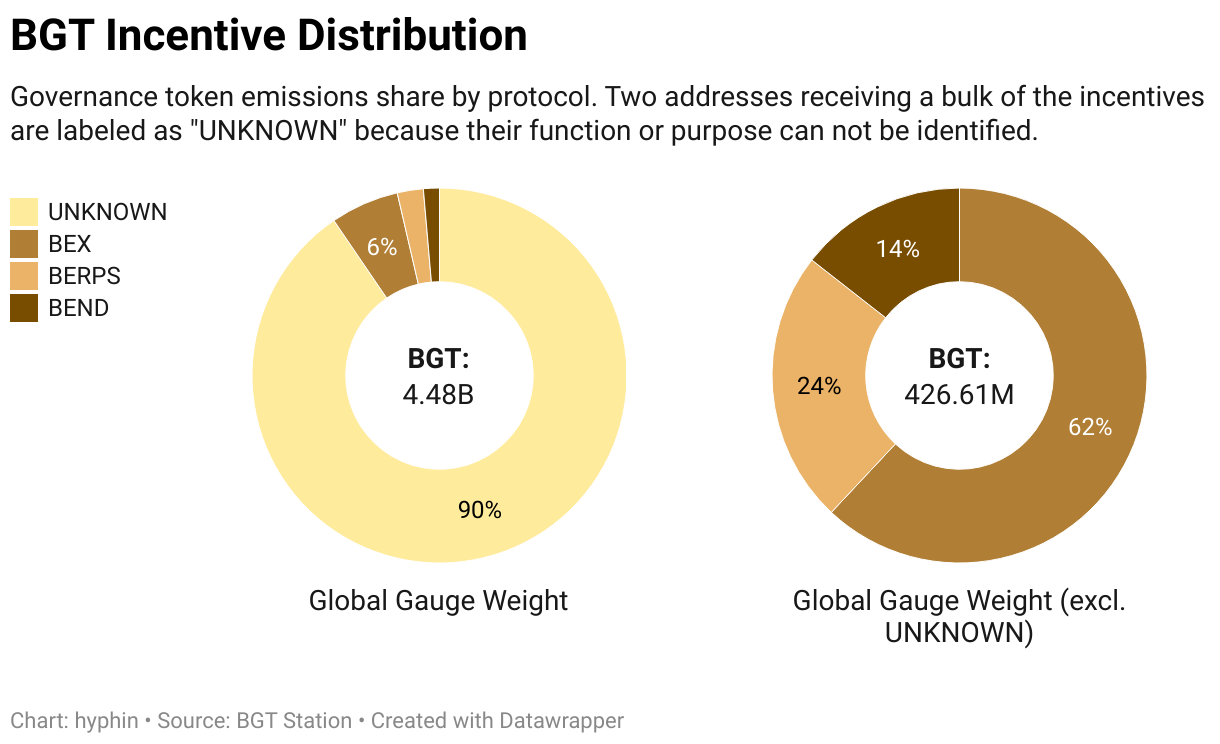

All delegation activity on Berachain is conducted via BGT Station, which houses all the relevant information about validators and facilitates BGT > BERA conversions. Querying validator data allows us to pinpoint the emissions routes and weights in order to establish what is prioritized by the governors.

It’s uncertain where most of the emissions are routed due to a lack of transparency, but it would make sense that these addresses are just placeholders as they’re not included in any readily available documentation and have no relevant recorded activity. We can ignore those unknowns for the time being and focus on what we can accurately observe.

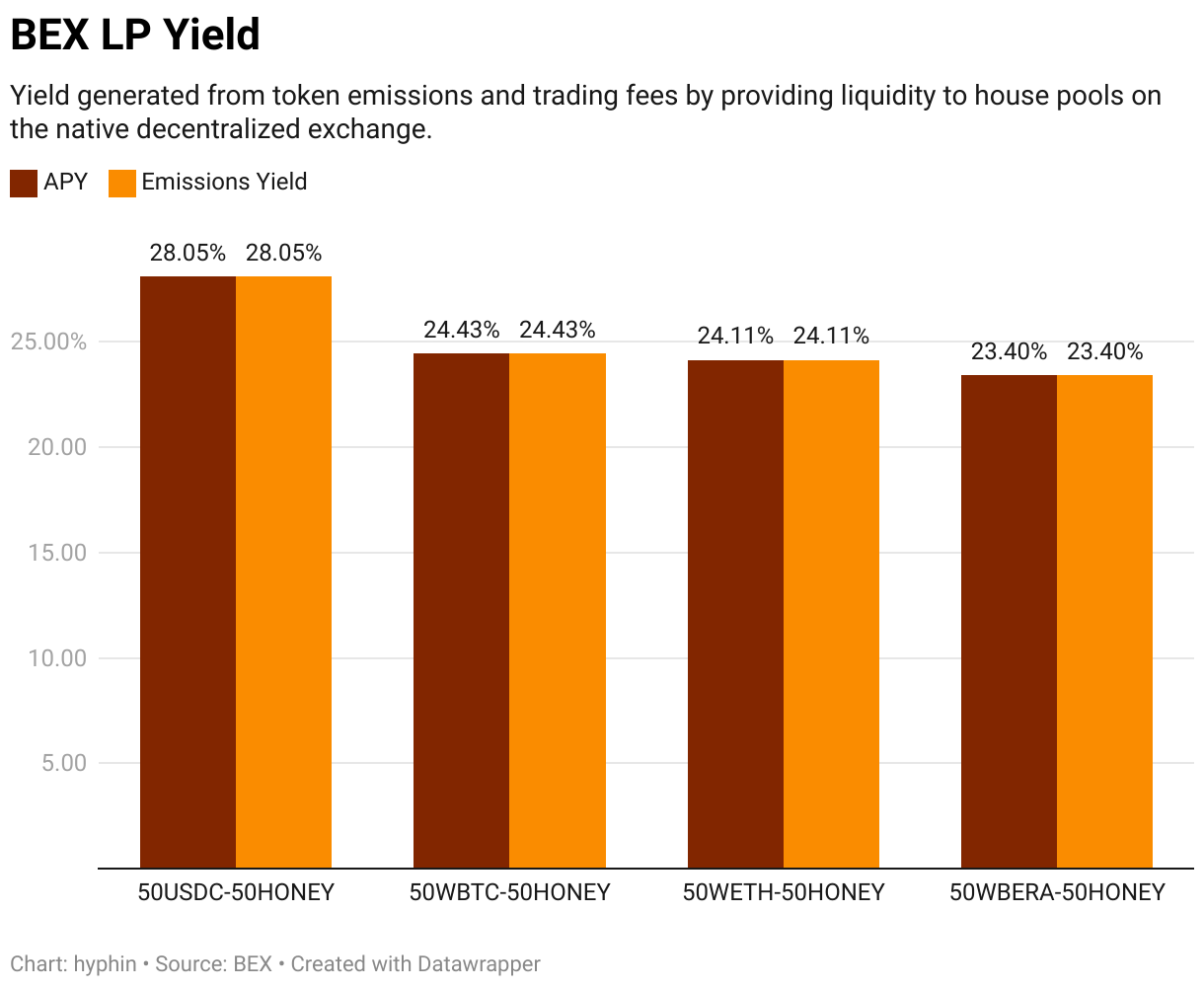

As expected, the native decentralized exchange receives the most amount of incentives, which are funneled into the four main house pools deployed alongside the protocol. Encouraging the use of protocols through inflation is also reflected in the global gauge weight chart, with BEND and BERPS offering additional benefits to depositors.

Yields for providing liquidity on the decentralized exchange tend to stay in the 20% range, mostly from emissions but can vary based on trading volume.

BGT issuance for liquidity providers is based on the amount of tokens directed to a specific pool by validators, and the individual’s pool ownership percentage.

An important part of the ecosystem — bribes, are unfortunately not offered by any of the active validators and can’t be analyzed.

Conclusion

Innately being an experiment for educational and development purposes, it’s needless to say that the testnet launch was a success, campaign driven or not. Builders had a chance to stress test their products in an unpredictable environment and plenty of verifiable on-chain activity was logged in the process that could be used for research. There are definitely a lot of improvements to be made, especially when it comes to on-chain visibility and transparency in a data sense.

Mainnet

There isn’t an official launch date set in stone, but comments made by one of the founders hint at it going live within the next few months.

Improvements

Something to look forward to in the final release will be the utilization of fully functioning bribes and non-native protocols being able to receive a share of governance token incentives for bootstrapping initial liquidity. Everyone will also have a chance to run a validator node without being whitelisted (requirement for testnet validator nodes at the moment).

Will there be an airdrop?

Nobody knows for sure, although a lot of people speculate that there will be one. In case you ever see any links related to a Berachain airdrop, please don’t click them as they’re likely a scam.

Takeaway

It’s hard to predict how the mainnet deployment will play out exactly. The testnet was a great opportunity to see the proof-of-liquidity model in action, confirming that the team behind Berachain means business and is capable of delivering something novel. Heavy interest from builders looking to set up shop and oversubscribed funding rounds taking place behind the scenes indicate that a new narrative might be brewing.

Disclaimer: The information provided is for general informational purposes only and does not constitute financial, investment, or legal advice. The content is based on sources believed to be reliable, but its accuracy, completeness, and timeliness cannot be guaranteed. Any reliance you place on the information in this document is at your own risk. On Chain Times may contain forward-looking statements that involve risks and uncertainties. Actual results may differ materially from those expressed or implied in such statements. The authors may or may not own positions in the assets or securities mentioned herein. They reserve the right to buy or sell any asset or security discussed at any time without notice. It is essential to consult with a qualified financial advisor or other professional to understand the risks and suitability of any investment decisions you may make. You are solely responsible for conducting your research and due diligence before making any investment choices. Past performance is not indicative of future results. The authors disclaim any liability for any direct, indirect, or consequential loss or damage arising from the use of this document or its content. By accessing On Chain Times, you agree to the terms of this disclaimer.